Last month I had the pleasure of seeing Sarah Bauder present at the COHEAO Annual Conference in Pentagon City, VA. Sarah is Assistant Vice President for Enrollment Services and Financial Aid at the University of Maryland, College Park (which happens to be my alma mater - Go Terps!). Her presentation detailed the results of a comprehensive study on 10 years of student loan defaulters. The purpose of the study was to identify the characteristics which are associated with defaults, as well as to establish a strategy on how and where to use financial literacy education as a proactive solution.

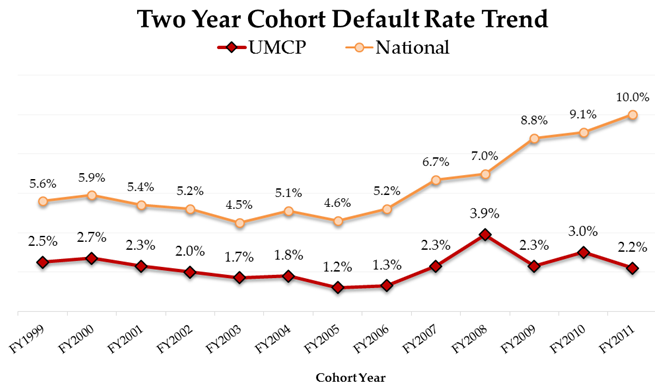

This graph shows the effect of UMCP's proactive solutions, as the University's default rate dropped substantially in 2009 when the national average rose 1.8%

Now, most of the time a presentation consists almost entirely of data, eyes will glaze over and iPhones will come to life. But during this presentation, all attendees were 100% engaged as the presentation was packed with alarming insights and astounding applications.

The study began with an extensive data warehouse project; data on academics, loan statistics, demographics and even campus activities were compiled for all student loan defaulters. Several trends emerged as certain characteristics continued to pop up for these former students.

Here are a few stats from the study:

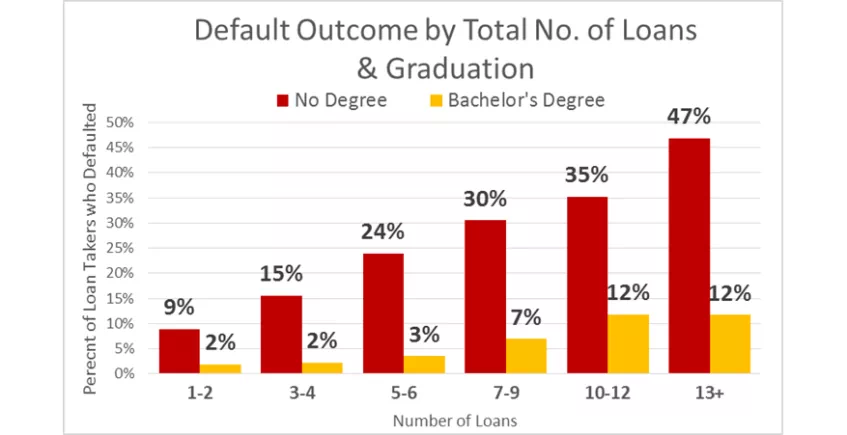

- Students that do not graduate had default rates more than 3.7 times higher than those that do graduate

- Independent students had default rates 2.3 times higher than dependent students

- Transfer students were more likely to default regardless of whether they graduate

- Almost one in five students with low high school GPA’s who did not graduate from college defaulted on their student loans

Unsurprisingly, the number one influencer was "not graduating". But more importantly, the data showed Bauder and her team which students were not graduating. The following factors were shown to be the biggest factors which increased the risk of default:

- Socio-economic barriers

- Independent filing status

- Students enrolled for 13terms

- “C” and below students

- Students with undeclared major

- Loans totaling over $20,000; with more than 10 loans

Graduating seems to mitigate almost all other risk factors for defaulting, so Bauder and her team focused on proactive solutions to improve the graduation rates for students who fit these profiles. Some of the initiatives included:

- Offering personalized counseling for loan borrowers with certain characteristics

- Incorporating personal finance education in the new student orientation course

- Enhancing the Satisfactory Academic Policy requirements

- Expanding the Senior Debt Cap Program

One of the most eye-opening parts of the presentation was seeing the short term results of these proactive solutions on UMCP’s student loan default rate. In 2009, when the national default rate rose a staggering 1.8% (the largest increase since 1989), UMCP’s default rate actually decreased by 1.6%!

There were several other excellent data conclusions and resulting initiatives within the presentation, but I don't have enough time or space to cover them all. If you would like to see all of the data, graphs and conclusions, you can download the full presentation here.